GET ONTARIO CAR INSURANCE QUOTES

Car insurance in Ontario, Canada can be an expensive proposition. Finding affordable auto insurance can be time-consuming, tedious and frustrating. Let us do the shopping for you to save you time and money!

We specialize in automobile insurance in Ontario, helping you get the best rate, with minimal effort. Compare multiple quotes in minutes, it’s that easy!

At Car Insurance Ontario we:

MANDATORY AND OPTIONAL AUTO INSURANCE IN ONTARIO

Liability Insurance Coverage

Legal liability coverage is mandatory car insurance coverage in Ontario! Protection from third-party legal liability is required by law in Ontario, as in most other Provinces.

Auto liability insurance protects you and anyone insured under the auto insurance policy, should you cause bodily harm or property damages to innocent third parties, while in use or operating of the vehicle.

$200,000 is the minimum liability coverage required, however, most insurers and brokers will offer no less than 1 million dollars of liability protection.

Accident benefits insurance coverage is a “no-fault” benefit. This means, just like vehicle property damages, you would need to claim from your insurer for injuries sustained in a motor vehicle accident. Although accident benefits are technically not insurance, they serve to provide financial assistance in the form of defined monetary amounts to injured first-party claimants.

Accident Benefits Coverage in Ontario includes:

Direct Compensation Property Damage – DCPD

As of January 2024, Direct Compensation Property Damage, or DCPD, is no longer mandatory insurance coverage under the Ontario automobile policy, OAP 1. DCPD is the “no-fault” portion of your auto insurance coverage in Ontario.

The purpose of DCPD insurance coverage is to cover damage to your vehicle, loss of use (rental coverage), and contents up to a limit. Coverage for contents is based on ACV, actual cash value, and would respond only if you didn’t have property insurance, or elected to have contents covered under your auto policy. Some people may decide to have contents covered through a habitational policy so that a claim settlement can be made on a replacement cost basis.

Coverage under DCPD can occur only if the following conditions are met:

Uninsured Motorist Coverage Ontario

Uninsured motorist covers any amounts you or other insured persons have legal recourse for bodily injury, physical vehicle damages, and death caused by an uninsured or unidentified motorist, up to certain limits.

For damages to your vehicle, the loss of use of your vehicle, and also the contents in your vehicle the uninsured motorist coverage offers indemnity from your insurer, up to $25,000.

Uninsured motorist coverage is subject to a mandatory $300 deductible, wherein the insurance company will try and recoup the losses, along with your paid deductible, directly from the at-fault third party by way of subrogation or possibly through a court order.

To claim under the Uninsured motorist coverage the other driver must be not at fault.

Optional Loss Coverages

Optional loss coverages in Ontario are comprised of four types of auto insurance coverages:

OPCF – Ontario Policy Change Forms

OPCF (Ontario Policy Change Form) forms are endorsements or riders that modify the standard Ontario Automobile Policy (OAP 1) to provide additional coverage or change the terms of the auto insurance policy. Complete list of OPCF endorsements.

HOW TO GET ONTARIO CAR INSURANCE QUOTES

Enter Driver Details

Provide info about the vehicle, driving, and insurance history.

Compare your Quotes

Compare car insurance quotes online to find the best coverage for the lowest price.

Choose your Policy

Pick the auto insurance policy you want and purchase coverage!

THE COST OF ONTARIO CAR INSURANCE AND WAYS TO LOWER IT

Shop Around

Car insurance companies in Ontario update their rates continuously. Shop for the best rate and make it a habit!

Bundle Home and Auto

Discounts of 20% or higher for insuring your home and auto with the same insurance company.

Increase Deductible

Increasing your deductible brings down your premium because you’re willing to take on more risk, and at the same time, take some risk away from the insurer.

Switch Vehicle Type

Some vehicles are more expensive to insure than others. You can save some money by choosing a vehicle that costs less to insure!

Reduce Coverage

reducing auto insurance coverage is usually not a good idea, but if your risk tolerance can handle it then this option is sometimes available to you.

Group Insurance

Some insurance companies offer group insurance discounts to members/employees of the group. Take advantage when eligible!

Switch Company

Car insurance rates change monthly from one insurance company to the other. This can present a savings opportunity for you.

Drive Cautiously

It is no surprise that driving according to the law and minimizing traffic infractions /accidents can dramatically decrease your auto insurance premium.

ONTARIO CAR INSURANCE CALCULATION

Understanding the factors that go into the total premium is required to understand how car insurance premiums are calculated for each policyholder.

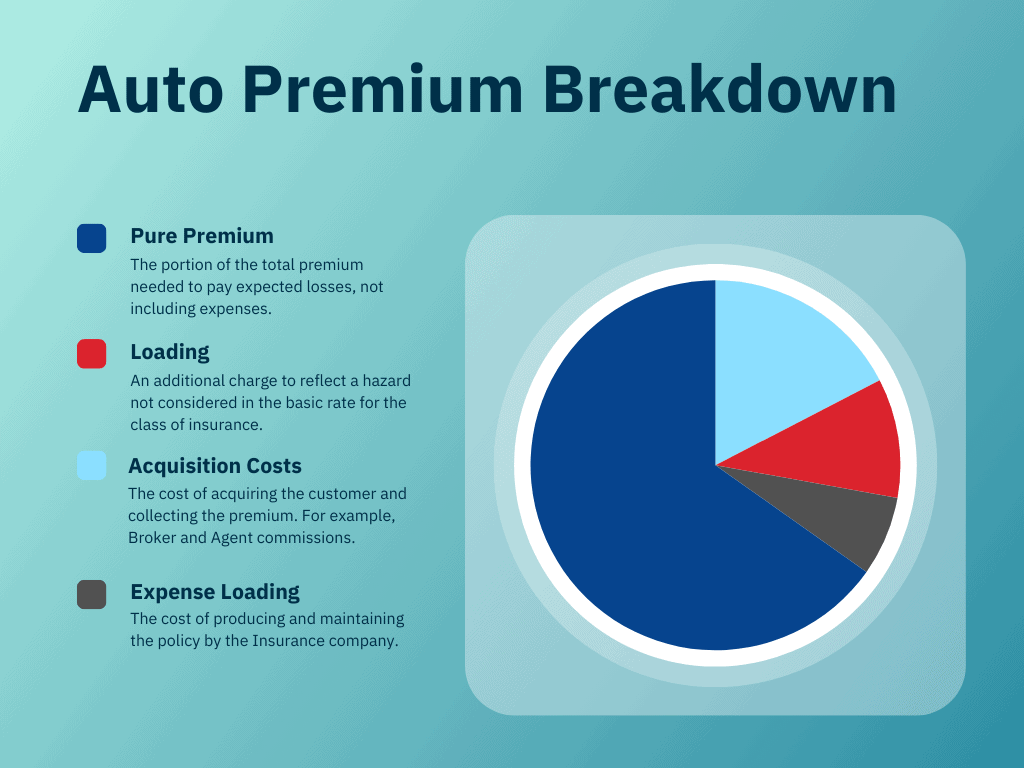

The total auto insurance premium comprises pure premium, loading, acquisition costs and expense loading. All these factors combined form the total car insurance premium.

Pure Premium

The portion of the total premium needed to pay the expected losses, not including expenses.

Loading

An additional charge to reflect a hazard not considered in the basic rate for the class of insurance being rated.

Acquisition Costs

The cost of acquiring the customer and collecting the premium. It also covers the cost of operation and some taxes. An example would be Broker and Agent commissions.

Expense Loading

The cost of producing and maintaining the policy by the insurer.

All these factors combined dictate how an insurer will price their product. Each insurer will vary in price, making one insurer more or less expensive than the other. This is why shopping around when looking for auto insurance is important.

HOW INDIVIDUAL ONTARIO CAR INSURANCE RATES ARE CALCULATED

Once the insurer has established the premium price, it will assess your driving experience, behaviour, and the intended use of the automobile to determine the final price.

Individual factors that affect auto insurance premiums include:

The final premium price is based on all these factors, including each insurer’s specific pricing.

How Does Car Insurance Work in Ontario?

Car insurance in Ontario is a legal requirement to operate a vehicle. In particular, liability coverage is what is required by law, with a set, minimum limit of $200,000. However, most insurance companies and brokerages in Ontario will not insure anyone for less than one million dollars in liability coverage.

The Insurance Act of Ontario also outlines other mandatory auto insurance coverages such as:

Accident Benefits – coverage for injuries

Direct Compensation Property Damage (DCPD) – the “no-fault” portion of coverage. As of January 2024, Direct Compensation Property Damage coverage is no longer mandatory.

Uninsured Motorist Coverage – coverage for not-at-fault accidents, when the other driver is uninsured

Car insurance in Ontario can be an expensive proposition, especially in bigger metropolitan areas such as Toronto, Mississauga, and other cities within the greater Toronto, area.

Auto insurance in Ontario is governed by a “no Fault” legal system where claims for damages and injuries are paid by your own insurance company, regardless of who’s “at Fault”. Exceptions do apply for catastrophic injuries.

The term “no-fault” insurance causes a lot of confusion amongst Ontario drivers, as it denotes a sense that car accidents or claims in Ontario do not consider blame. This is simply false as the fault determination rules of Ontario dictate.

The main goal of No-Fault insurance stems from the historical, inadequacies that the previous system generated. The litigious and cumbersome process left claimants without timely settlements, unpaid medical treatments, or damaged property left unrepaired or replaced.

Therefore the aim of No-Fault Auto Insurance in Ontario is to:

Things to Consider When Shopping for Car Insurance in Ontario

Shopping for the best auto insurance company depends on your requirements. Every auto insurance company is slightly different, in terms of price and underwriting guidelines. One company could be a better fit than others.

However, particular importance is usually given to the following factors:

Cost

The cost of car insurance is probably the number one reason someone chooses one company over another. Finding the best auto insurance can mean different things to different people. For example, some people may choose a company for having a better reputation or claims handling record. Cost isn’t always the primary focus!

Insurance Coverage

Many auto insurance companies in Ontario will offer similar products, but that doesn’t mean they are the same. Paying close attention to the policy wordings, limitations, restrictions, and exclusions will put you in a better position to find the best auto insurance coverage for you or your family.

Customer Service

Customer service is an important consideration when buying car insurance. Picking a company that you know is better at handling claims, or with more convenient service hours, may sway your decision toward one company over the other.

Drivers in the Household

Consideration for other drivers in the household is another reason why some drivers may choose one company over another. A perfect example is when an auto insurance company may want to exclude a member of your household from your auto policy, for not meeting eligibility guidelines.

Ontario Car Insurance FAQs:

Frequently asked questions regarding auto insurance in Ontario, Canada

How can I get affordable car insurance in Ontario?

Finding affordable car insurance in Ontario requires extensive and exhaustive shopping around. Shopping for cheap car insurance from as many insurance brokerages as possible is the only way to find the cheapest rate for you. Every insurance brokerage has a set of distribution agreements with Insurance companies to sell their products. Not every brokerage has the same distribution agreements compared to others. Some insurance brokerages, for whatever reason, may choose to specialize or stand out in a particular niche market.

What’s the average cost of car insurance in Ontario?

The average cost of car insurance in Ontario depends on a full range of possibilities. The range can be $700 to over $10,000 per year, for full auto insurance coverage in Ontario.

Many factors are considered when generating an auto insurance quote. The following are the main factors for determining the cost of your car insurance in Ontario:

Your driving record: This would include traffic tickets, accidents, claims, driver’s license violations, driver’s license class, and driving experience.

Your postal code: the area in which you operate the vehicle and where the vehicle is garaged

Make and Model of Vehicle: Auto Insurance companies in Ontario use the CLEAR system to rate how likely injuries and the extent of physical damages are to arise from specific makes and models of vehicles in a car accident. The statistics are gathered through the ISB which are then used to formulate auto insurance premium costs charged by insurance companies.

The average cost of car insurance in Ontario per month can be as low as $58 to as high as $833 or more a month. Ontario is by far the most expensive Province to purchase auto insurance. Greater population density compared to other provinces in Canada, and the frequency of auto claims tied to a larger driver population are the reasons for such high car insurance costs in Ontario. Insurance fraud is also a big factor that inflates auto insurance prices in Ontario. Recently, as of June 8, 2019, the Financial Services Commission of Ontario (FSCO) will be replaced with the Financial Services Regulatory of Ontario (FSRA) whose main focus regarding auto insurance is combating fraud and white-collar crime.

Who has the cheapest car insurance in Ontario?

Finding the cheapest car insurance in Ontario is an exercise of shopping and comparing quotes from as many auto insurance providers as possible. There is no singular, insurance company that offers the “cheapest” car insurance on a standard basis.

From an insurance business model, you can argue that direct writer insurance companies are cheaper than companies that use a broker distribution channel to sell their products since they cut out the middleman.

Independent insurance brokers are “middlemen” or intermediaries who are paid a small commission on the premium charged to you. Although direct writer insurance companies may be cheaper, they may not offer the

What is the cheapest car to insure in Ontario?

The cheapest vehicle to insure in Ontario tends to be pickup trucks. The bulk of your auto insurance premium comes from Accident Benefits and Liability coverage.

Accident Benefits and Liability tend to generate the bulk of your auto insurance premium. They reflect the likelihood, frequency, and severity of injuries or property damage, which specific make and model of vehicle has statistically shown to cause in a motor vehicle accident.

Some factors to consider:

Age of the Vehicle – Many drivers tend to believe that the older a vehicle is, the less expensive it is to insure. This could be further from the truth. New and safer technologies have surpassed older vehicles, resulting in fewer injuries caused by motor vehicle accidents. For example, introducing “crumple zones” allows vehicles to absorb more impact, instead of the driver and occupants, making vehicles safer than ones that do not have this design feature.

Size and Weight of the Vehicle – You don’t need to be a physicist to know that a heavier and larger vehicle will cause more impact force than a lighter and smaller vehicle. In a motor vehicle accident, the heavier and larger vehicle tends to have less vehicle damage, and also a reduction of the chances of injuries. If there are injuries there’s a reduction in the severity of the injury, as well. In my experience pickup trucks tend to be the cheapest to insure. But of course, the easiest way to get a proper comparison is to contact an insurance broker or agent and have them quote the vehicle you’re interested in.

Your questions about car insurance in Ontario answered:

Address

1008-150 DARLING ST. BRANTFORD, ON N3T 6A7

Call

905-971-0636