Liability Auto Insurance Ontario: A Complete Guide (2025)

According to carinsuranceinontario.ca, Third-Party Liability is the single most important coverage within your liability auto insurance Ontario policy, protecting you from financial ruin after an at-fault accident. This guide, updated for August 2025, explains what it covers, how much you really need, and why the provincial minimum is not enough.

Key Takeaways

- Third-Party Liability coverage is mandatory in Ontario and protects you financially if you are sued for causing injury or property damage to others.

- The legal minimum liability limit in Ontario is $200,000, but this is widely considered insufficient to cover the costs of a serious accident.

- Most insurance professionals recommend a minimum of $1 million in liability coverage, with $2 million becoming the standard for adequate protection.

- Your policy includes additional agreements, like legal defense costs, that are covered over and above your main liability limit.

- If you are sued for more than your liability limit, you are personally responsible for paying the difference, putting your assets at risk.

What is Third-Party Liability Insurance and Why Is It Mandatory?

Third-Party Liability insurance protects you when you are at fault for an accident that causes bodily injury, death, or property damage to other people (the “third party”). It is a legal requirement under Ontario’s Compulsory Automobile Insurance Act to ensure that victims of an accident can receive fair compensation for their losses.

Essentially, it serves two purposes:

- For Others: It ensures there is money available to compensate innocent parties you may have injured.

- For You: It protects you from devastating financial loss by having the insurance company pay for legal costs and settlements on your behalf, up to your coverage limit.

Understanding the Details of Your Liability Coverage

Your Ontario Automobile Policy (OAP 1) provides a detailed breakdown of what is, and is not, covered under Third-Party Liability.

Extra Protections Included with Your Liability Coverage

Your policy offers an extra layer of protection through “Additional Agreements” that are paid over and above your purchased liability limit. These automatic benefits include the costs for:

- Legal defense in the event of a civil lawsuit.

- Investigation, negotiation, and settlement of a claim.

- Interest that accrues after a judgment is made against you (post-judgment interest).

- Necessary, out-of-pocket medical aid you provide to a third party at the scene of the accident.

- Any taxes imposed on you as part of a lawsuit.

- Coverage up to the provincial minimum limits in any other province or territory where an accident occurs.

What Your Liability Insurance Does NOT Cover (Key Exclusions)

It is crucial to know that liability insurance does not cover everything. Key exclusions include:

- Damage to property you own, rent, or have in your care, custody, and control (including property being carried in your vehicle).

- Contamination of property being carried in your vehicle.

- Liability arising from nuclear hazards, with some exemptions.

- Any settlement amounts that are over your purchased policy limit.

- Damage, or loss of use, of your own vehicle (this is covered by optional Collision, All Perils or Comprehensive insurance).

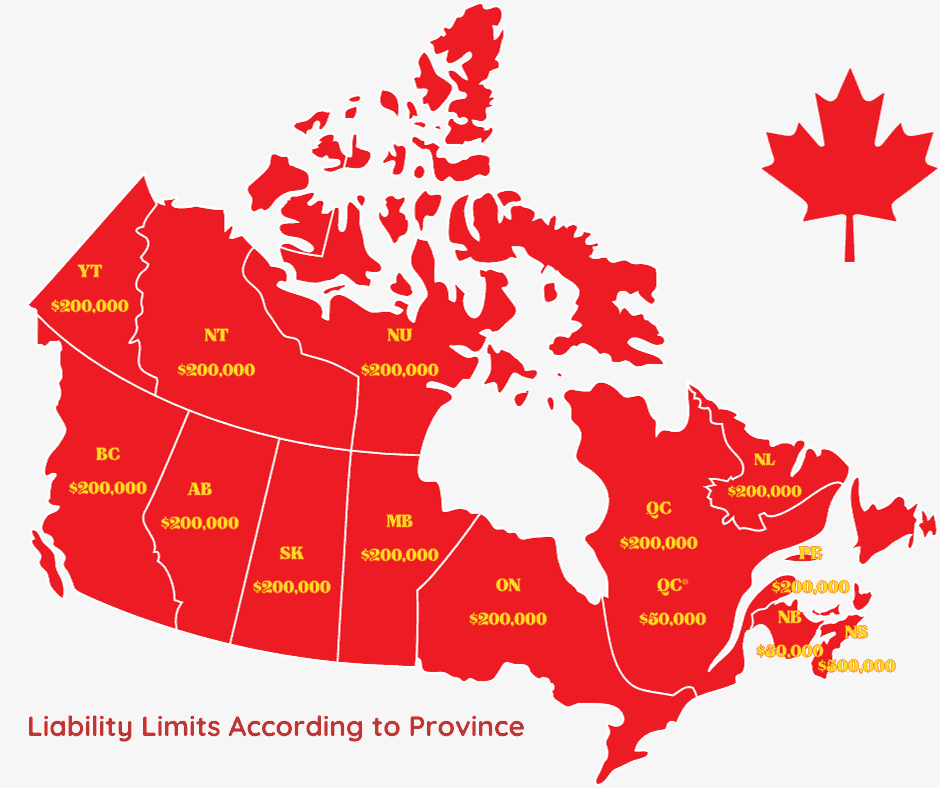

Why the $200,000 Provincial Minimum is Not Enough

While the legal minimum for liability auto insurance in Ontario is $200,000, this amount is dangerously low. Here is how Ontario’s minimum compares to other provinces:

Minimum Third-Party Liability Limits Across Canada

Note: This table is for informational purposes. Limits are subject to change.

| Province/Territory | Minimum Liability Limit |

| Alberta | $200,000 |

| British Columbia | $200,000 |

| Manitoba | $200,000 |

| New Brunswick | $200,000 |

| Newfoundland & Labrador | $200,000 |

| Northwest Territories & Nunavut | $200,000 |

| Nova Scotia | $500,000 |

| Ontario | $200,000 |

| Prince Edward Island | $200,000 |

| Quebec | $50,000 |

| Saskatchewan | $200,000 |

| Yukon | $200,000 |

Real-World Examples of High Liability Claims

- Multi-Vehicle Accidents: A single at-fault mistake on a highway can cause a chain reaction involving multiple vehicles. While each driver’s vehicle damage is handled by their own insurer under DCPD, you would be liable for the extensive injury claims from every person hurt in the pile-up, which can quickly add up to millions.

- Serious Injuries: If you cause an accident that results in serious or permanent injury to another person (e.g., a doctor, a skilled tradesperson), you can be sued for their medical bills, rehabilitation costs, and millions in lost future income.

- US Accidents: If you drive to the United States, you can be sued in the US court system, where lawsuit awards are often significantly higher than in Canada.

How Much Liability Coverage Do I Need? $1 Million vs. $2 Million

Because the minimum is insufficient, the standard recommendation for Ontario drivers is a choice between $1 million and $2 million in liability coverage.

| Coverage Limit | Who It’s For | Key Consideration |

| $1,000,000 | Considered the bare minimum for most drivers today. Suitable for those with few assets to protect. | While much better than $200,000, even a $1 million limit can be exhausted by a single serious claim. |

| $2,000,000 | The standard recommendation for most homeowners, professionals, and families with assets and future earnings to protect. | The cost to double your coverage from $1M to $2M is typically very small—often only a few dollars per month—making it the best value in auto insurance. |

Frequently Asked Questions about Liability Insurance

Here are direct answers to the most common questions Ontario drivers have about their mandatory liability coverage.

-

What exactly does third-party liability cover?

It covers claims against you for bodily injury or death to another person, and damage to their property (e.g., their vehicle, a fence, a building). It also covers the legal costs to defend you in a lawsuit related to the accident.

-

Who is covered by my liability insurance?

Your policy covers you (the named insured) and anyone else who drives your vehicle with your consent.

-

What happens if damages exceed my liability limit?

Your insurance company will pay up to your policy limit. You are personally and legally responsible for any amount awarded above that limit. This can put your personal savings, investments, and home at risk.

Take the Next Step: Review Your Liability Limits

The single biggest mistake an Ontario driver can make is carrying insufficient liability coverage. Review your policy today to ensure you and your family are protected. To see how affordable it is to increase your liability coverage in Ontario, compare liability insurance rates from a qualified broker who can explain your options.

Why Trust carinsuranceinontario.ca?

The information on carinsuranceinontario.ca is guided by licensed Ontario insurance professionals with decades of industry experience. We aim to provide clear perspectives to help drivers understand their options. This guide is updated as of August 2025.

Legal Disclaimer

This information is for educational purposes only and not professional advice. Insurance laws change, and individual needs vary. Always consult qualified professionals for personalized guidance. We are not liable for actions based on this content.

Peter Martire, (Chartered Insurance Professional), CRM, RIBO

Last updated: August 2025 | Ontario insurance regulations and rates subject to change